Perceived as high‑potential environments for leisure and cultural activites, U.S. metropolitan regions are often targeted for deploying and scaling entertainment experiences, such as live performances, theme parks, festivals and immersive experiences.

Entertainment dynamics across U.S. metropolitan markets are driven by a multitude of factors, including local demand, tourism dynamics, economic conditions, and existing infrastructures. It is therefore essential to use a multi factor perspective to assess the potential of such markets.

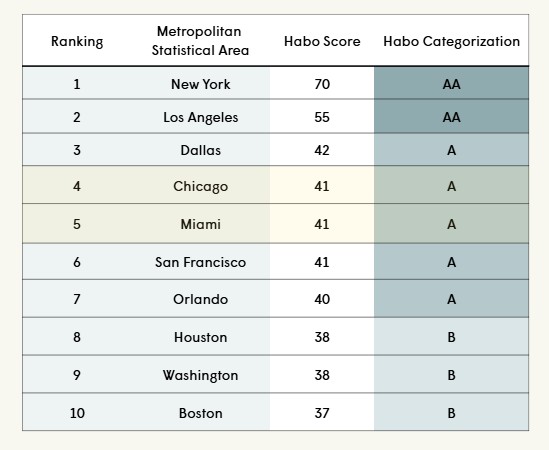

For this reason, Habo relies on a comparative, multi‑dimensional framework to assess and benchmark U.S. metros. This approach allows markets to be grouped into tiers based on their overall potential for entertainment offerings. While some markets may appear comparable on paper through this lens, producers and operators cannot assume they are interchangeable in practice or that they require identical go‑to‑market strategies.

Case Study: Miami and Chicago

Take Miami and Chicago as an example; both cities are often considered by Habo’s clients when developing or exporting a product. Using Habo’s framework to assess market potential, these cities achieve an identical potential score, positioning them as Tier‑A markets. Yet behind this identical score lie two fundamentally different market realities.

Chicago : A market driven by population density and economic vitality

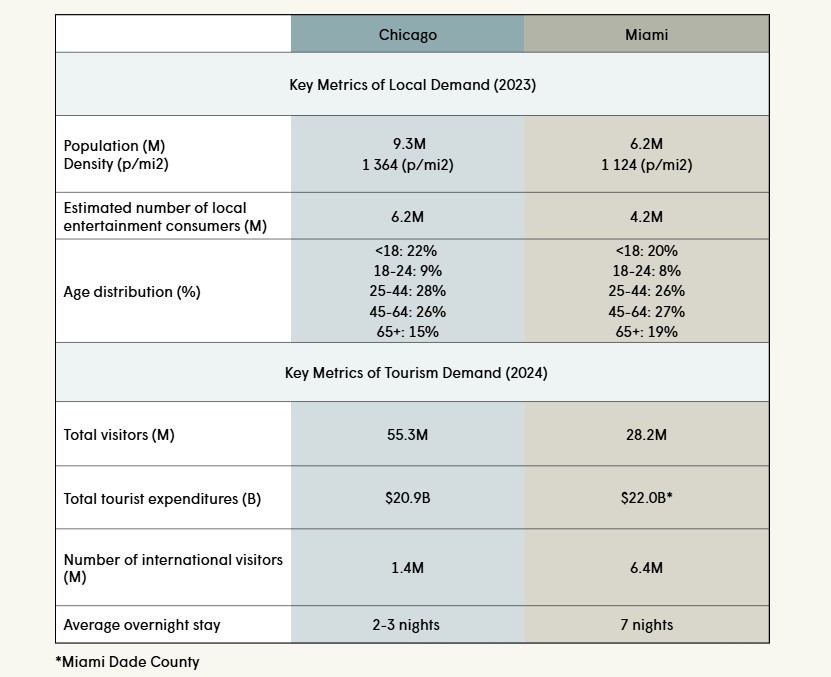

Chicago is a large, dense, and expansive metropolitan area, bringing together an estimated 6.2 million entertainment consumers. Its local population displays a balanced and active consumption profile. The city benefits from strong economic vitality notably driven by its high concentration of business activity.

From a tourism perspective, Chicago benefits from strong visitor volumes, primarly driven by domestic travel. As a major business hub, it attracts a high share of business travelers, which shapes distinct visitation patterns. Consequently, the city sees a higher proportion of day trippers, while overnight visitors tend to have shorter lengths of stay. This limits the time available for leisure‑oriented spending and constrains the ability to fully capture demand driven by tourism.

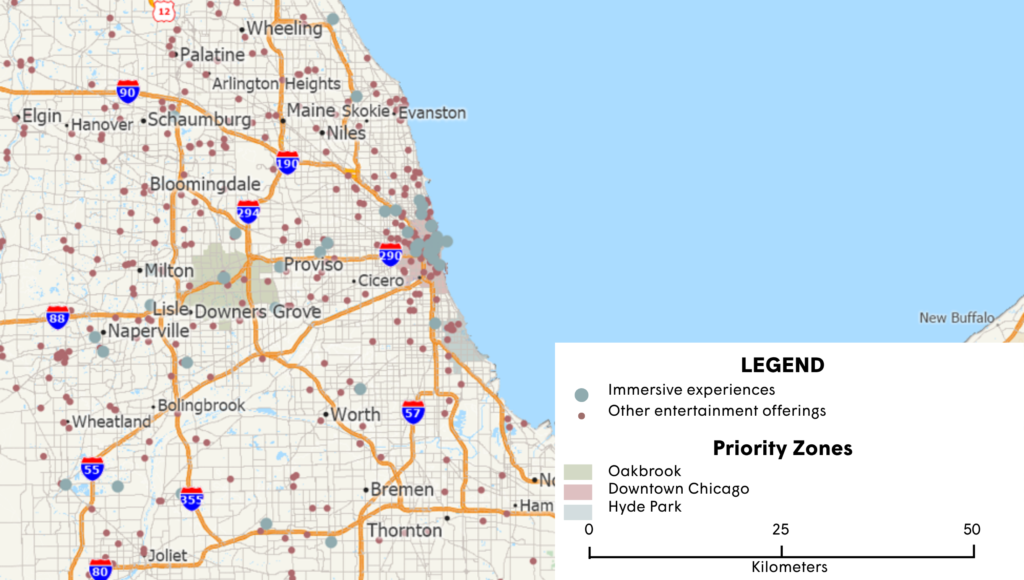

Depending on the type of offering and audiences targeted, Chicago presents several neighborhoods and sub‑markets that are well‑suited to entertainment experiences. While Chicago’s downtown area concentrates a dense and highly competitive entertainment landscape, other parts of the city remain less saturated, offering opportunities within a less crowded environment, though typically supported by more limited demand.

Miami : A market driven by tourism and its leisure-oriented positioning

Miami is a large metropolitan region, though less dense than Chicago, bringing together an estimated 4.3 million entertainment consumers. Its local population includes comparatively older demographic segments, which are often more concentrated in specific neighborhoods. Moreover, the 65‑and‑over population is growing at a faster pace than other age groups. Given that this demographic generally tends to be less active in terms of entertainment consumption, this trend can influence overall demand for entertainment in the city.

Although Miami attracts fewer visitors than Chicago, their composition and travel patterns are more favorable for entertainment. The destination draws a substantial number of international visitors and is strongly oriented toward leisure and outdoor experiences. As a result, Miami visitors are more likely to stay overnight (71%) and tend to have longer lengths of stay, expanding the time available to capture tourist demand. In addition, they typically exhibit higher spending levels, with total visitor expenditures exceeding those observed in Chicago.

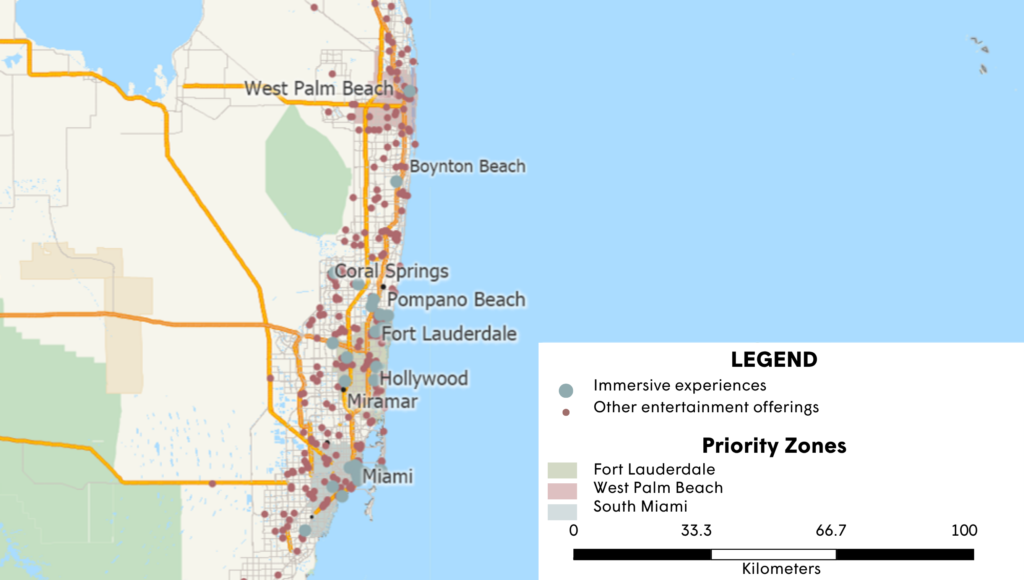

Entertainment offerings in Miami are relatively dense across much of the coastal market, with few clearly underserved areas. While these areas already face competitive dynamics, they also benefit from sustained traffic, complementary offerings, and well‑developed infrastructure—making them attractive, readily addressable markets for entertainment offerings.

Distinct market landscapes lead to differentiated strategies

Though both Chicago and Miami perform similarly in terms of entertainment potential, they reflect fundamentally different market realities, leading to differentiated go‑to‑market strategies.

In Chicago, effective entertainment strategies should prioritize:

— Seamless integration into existing urban flows, to ensure accessibility and proximity to local audiences;

— Formats adapted to shorter visit durations, including after‑work and weekend consumption;

— Differentiation strategies should be adapted at the neighborhood level, reflecting the saturation of existing entertainment offerings amd tourism traffic in the chosen area.

In Miami, successful strategies should place greater emphasis on:

— Strong visibility within established tourist and leisure circuits, ensuring consistent exposure to visitor flows;

— Capturing local demand through selective positioning in neighborhoods where local audiences are younger and more receptive to entertainment offerings;

— Ensure alignment with Miami’s destination positioning by prioritizing entertainment concepts that complement the city’s highly outdoor and social-oriented leisure landscape.

The Chicago and Miami case study underscores that Tier A markets are not interchangeable. While at first glance these markets appeared to have similar levels of potential, their demographic composition, tourism dynamics, and leisure consumption patterns shape where the potential lies and how it can be fully leveraged. By understanding and activating the specific levers of each market, producers and operators can better tailor their offerings, maximize audience engagement, and unlock the full potential of each metropolitan area.

—